In the realm of inventory accounting, two prominent methods for valuing inventory are LIFO (Last-In, First-Out) and FIFO (First-In, First-Out). Both LIFO and FIFO play significant roles in determining a company’s financial statements and tax obligations. Understanding these inventory valuation methods and their implications is crucial for businesses seeking to optimize their financial strategies and make informed decisions.

In this exploration of “What Is LIFO? Is LIFO Better Than FIFO?” . We will delve into the fundamental concepts of LIFO and FIFO, examining their respective advantages, disadvantages. We also explore the impact they can have on a company’s financial performance.

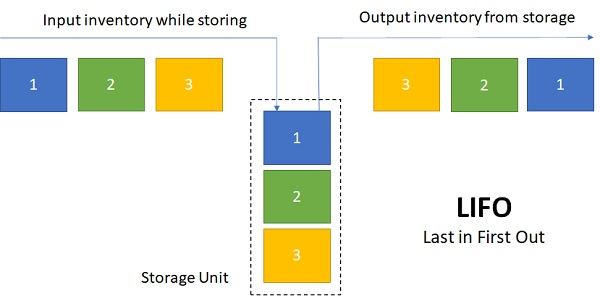

What is LIFO?

LIFO stands for “Last-In, First-Out,” and it is an inventory accounting method used to determine the cost of goods sold (COGS) and the value of ending inventory. Under the LIFO method, the assumption is that the most recently acquired or produced items in inventory are the first to be sold. In other words, the last items added to the inventory are considered to be the first ones sold, hence the name “Last-In, First-Out.”

Pros and Cons of LIFO

Pros of LIFO

Tax Advantages in Inflationary Periods

LIFO can lead to lower reported profits and, consequently, lower income tax liabilities during periods of inflation. By matching higher current costs with revenue, LIFO results in higher COGS, reducing taxable income and deferring tax payments.

Cash Flow Benefits

Lower tax payments under it can provide businesses with increased cash flow, which can be reinvested in the company, used for expansion, or to fund other operational needs.

Simple to Understand and Implement

It follows a straightforward principle of selling the most recently acquired or produced items first, making it relatively easy to understand and implement, especially in industries with minimal inventory fluctuations.

Cons of LIFO

Inventory Layering and Obsolescence

It can lead to the creation of inventory layers, especially during rising prices, where older, lower-cost items remain in the balance sheet. This can result in complexities in managing inventory and potentially render some stock obsolete.

Distorted Financial Statements

It may not accurately reflect the current value of inventory, as the cost of goods sold is based on older, potentially outdated prices. This can lead to distorted financial statements that do not provide a true representation of a company’s financial position.

Higher COGS in Non-Inflationary Periods

In times of stable or declining prices, It can result in higher COGS compared to other inventory valuation methods like FIFO. This can lead to reduced gross margins and profitability.

In what cases is LIFO used?

Here are five scenarios where LIFO is commonly used:

Inflationary Economies

LIFO finds widespread use in countries experiencing high inflation rates. In such economies, prices of goods and materials tend to rise over time. By matching the higher recent costs with revenue, leads to higher Cost of Goods Sold (COGS), resulting in lower reported profits. This, in turn, allows businesses to defer taxes, providing a tax advantage during inflationary periods.

Manufacturing Industries

It is prevalent in manufacturing industries that deal with raw materials or components subject to price fluctuations. As costs of materials change over time, using helps allocate the most recent expenses to sales, providing a more accurate representation of production costs and profitability.

Perishable Goods

Businesses dealing with perishable items, such as food and pharmaceuticals, often opt for LIFO. The rationale behind this choice is to sell the most recently acquired or produced items first, ensuring that older stock is sold before it expires. By preventing spoilage and wastage, helps maintain product quality and reduces losses due to obsolescence.

Oil and Gas Industry

In the oil and gas sector, where the prices of crude oil and other commodities can be volatile, LIFO can be beneficial for managing inventory costs and profitability. Fluctuating prices of oil and gas reserves necessitate a method like LIFO to accurately match revenues and expenses.

Declining Prices

Although LIFO is known for its advantages in inflationary environments, it can also be useful when prices of goods are declining. In cases of deflation or falling prices, using can help avoid higher COGS associated with other inventory valuation methods like FIFO (First-In, First-Out).

While LIFO offers certain advantages in the aforementioned cases, its adoption may also introduce complexities. One of the primary challenges is the potential creation of inventory layering, especially during periods of rising costs. Older inventory layers may become obsolete or difficult to manage, leading to potential inefficiencies and increased carrying costs.

Moreover, it is essential to consider the accounting and tax regulations in the respective jurisdiction. Some countries may have specific rules that restrict or prohibit the use of LIFO for financial reporting purposes.

LIFO vs FIFO

LIFO (Last-In, First-Out) and FIFO (First-In, First-Out) are two contrasting inventory accounting methods. They are used to determine the cost of goods sold (COGS) and the value of ending inventory. They have different approaches to valuing inventory, which can significantly impact a company’s financial statements and tax liabilities. Let’s compare LIFO and FIFO based on several key aspects:

Inventory Valuation:

- LIFO: Under LIFO, the assumption is that the most recently acquired or produced items are the first ones sold. As a result, the COGS is based on the cost of the most recent inventory, while the ending inventory consists mainly of older, potentially lower-cost items.

- FIFO: With FIFO, the assumption is that the first items acquired or produced are the first ones sold. Consequently, the COGS is based on the cost of the oldest inventory, and the ending inventory mainly consists of the most recently acquired or produced items.

Financial Impact:

- LIFO: In times of rising prices, It can result in a lower reported profit compared to FIFO. This is because the higher cost of the most recently acquired inventory is matched with revenue. It leads to higher COGS and lower net income. As a result, can help companies defer taxes.

- FIFO: In contrast, FIFO tends to result in a higher reported profit during inflationary periods. s the older, potentially lower-cost inventory is matched with revenue. It leads to lower COGS and higher net income. This could result in higher tax liabilities.

Inventory Layering:

- LIFO: can create inventory layering, especially during periods of rising costs, where older layers of inventory remain on the balance sheet. It to complexities in managing inventory and potentially obsolete stock.

- FIFO: FIFO generally does not encounter the same inventory layering issue, as the oldest inventory is assumed to be sold first, reducing the complexities associated with managing older inventory layers.

International Use:

- LIFO: LIFO is commonly used in countries with significant inflation as it provides tax advantages by reporting lower profits.

- FIFO: FIFO is more widely accepted globally and is often required for financial reporting in many countries.

Ease of Record-keeping:

- LIFO: LIFO can be more complex to implement and track, especially during periods of fluctuating prices, as it requires precise record-keeping of the acquisition costs of individual inventory items.

- FIFO: FIFO is generally considered easier to manage since it follows a straightforward principle of selling the oldest items first.

In conclusion, while LIFO offers tax advantages in inflationary environments and can be relatively simple to understand, it also comes with challenges related to inventory layering, financial distortion, and potential limitations on its use. Businesses must carefully consider their industry, inventory dynamics, and financial objectives before deciding to use the LIFO method.